(AGENPARL) - Roma, 20 Marzo 2026 -

(AGENPARL) - Roma, 20 Marzo 2026 -

This post by Jeff Bolyard, Principal, Energy Supply Advisory, is featured in our March 2024 Monthly Monitor, which includes articles and analysis for the natural gas, electric, crude oil, and sustainability markets. To read the full newsletter, click here. To sign up for the Monthly Monitor distribution list, click here.

This post by Jeff Bolyard, Principal, Energy Supply Advisory, is featured in our March 2024 Monthly Monitor, which includes articles and analysis for the natural gas, electric, crude oil, and sustainability markets. To read the full newsletter, click here. To sign up for the Monthly Monitor distribution list, click here.

“Back in the day” is a term that refers to a past period of time – often many years ago – that generally describes how things used to be. Natural gas production strategies back in the day were very different from what they are today. Long gone is the producer wildcatter mentality that chased the next big production well with extremely high debt to offset a U.S. market that, at the time, needed LNG imports to meet demand. Indeed, times have changed.

Since 2010, domestic natural gas production has increased by 50%, and the U.S. gas market has flipped from a deficient supply/demand balance to a surplus, exporting 13.3 Bcf per day of LNG and another 5.7 Bcf/day to Mexico in February. This cosmic shift, along with the uncertain political and regulatory landscape of fossil fuels in general, has forced producers to shift their business strategies. The high-investment, high-debt, high-risk model has shifted in the past few years to a more cautious financial model that improves cash flow, rewards loyal stockholders, and lowers debt.

This “new producer” mindset has paid off during the extreme volatility that energy markets have experienced. However, the biggest wild card that remains in the market and that impacts domestic pricing continues to be weather, which requires storage to meet the peaks and valleys of demand. However, the 50% increase in production mentioned above has not been matched with a commensurate increase in the amount of storage, which has grown by just 10% over that period.

While the surplus in storage dwindled to just 113 Bcf to the 5-year average during winter storms Gerri and Heather in January, February 2024 ended up being the third warmest month on record – 7.2°F above normal temperatures and ballooning up the current surplus to 682 Bcf. With the inevitable arrival of spring and winter in the rearview mirror, the oversupplied market had nowhere to put the record production. Prompt March NYMEX contract – the last month of winter – settled at just $1.615/Dth and April settled on 3/26 at just $1.575. Both settlements had the lowest final settlement prices for these two months since 1995, which has compelled producers to react or risk having already unsustainably low prices drop even further.

This is when the new producer strategy came into play, as 2024 guidance started coming out earlier this month from producers. Maximizing cash flow is still a high priority in 2024 – in a lower revenue stream scenario, a vast majority of gas-weighted E&Ps have announced cuts to capital expenditures, removing $1.5 billion from 2024 budgets vs. 2023. Chesapeake Energy reported a 31% decrease in capital expenditures with plans to reduce production while negotiations to merge with Southwestern Energy continue. Production will likely be reduced even further once the deal closes.

Coterra, Comstock, Antero, CNX, and Ascent have all reported plans to significantly reduce investment and/or production this year. Even EQT, which will be able to relieve pent-up Appalachian production when Mountain Valley Pipeline (MVP) opens up in the near future, has announced a temporary shut-in of 1 Bcf per day for an undefined period due to the low-price environment. However, this will likely end when MVP opens.

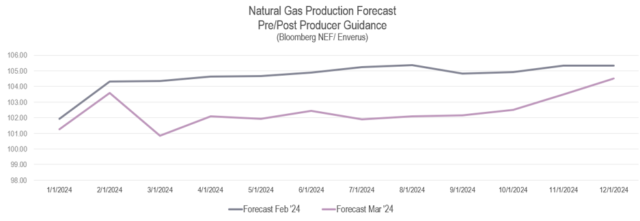

The result of these announcements is beginning to materialize in the form of lower production volumes being reported, as well as forecasts through the end of the year. In the chart below (data source: Bloomberg NEF/Enverus), the 2024 natural gas production forecast in February averaged 104.65 Bcf per day. After combining the impact of reduced capex and production volumes from the overall E&P group, the March forecast dropped that average by 2.26 Bcf per day. In total, it would remove 823 Bcf of natural gas from the market this year.

If this forecast becomes reality, the change in producer strategy to reduce investment and production guidance will not only help ensure the longer-term viability of their companies by preventing the current low-price environment from going even lower. It will also protect the all-important pipeline and storage infrastructure from being oversupplied and over-pressured, as well as make it better prepared for next winter when, like every winter, it all resets and weather once again becomes the driver of natural gas prices.

Contact Trio today to learn more!

The post Low Natural Gas Prices Spur a Different Producer Strategy appeared first on Edison Energy.

(AGENPARL)